Franchise Sellers Are Allowed to Lie (Mike Gould – Hounds Town USA Franchise) Part 2

Many prospective & current franchisees incorrectly assume that, if they are blatantly lied to, fraudulently induced or otherwise treated unfairly,

Read More

No-Nonsense Hype-Free Franchise Issues & Discussion Site

Many prospective & current franchisees incorrectly assume that, if they are blatantly lied to, fraudulently induced or otherwise treated unfairly,

Read More

Hounds Town USA has registered William “Bill” Wotochek as their franchise sales representative and broker. Bill Wotochek is a franchise

Read More

Franchise sellers claim that “buying” a franchise is a safer path to business ownership since franchising is “highly regulated.” The

Read More

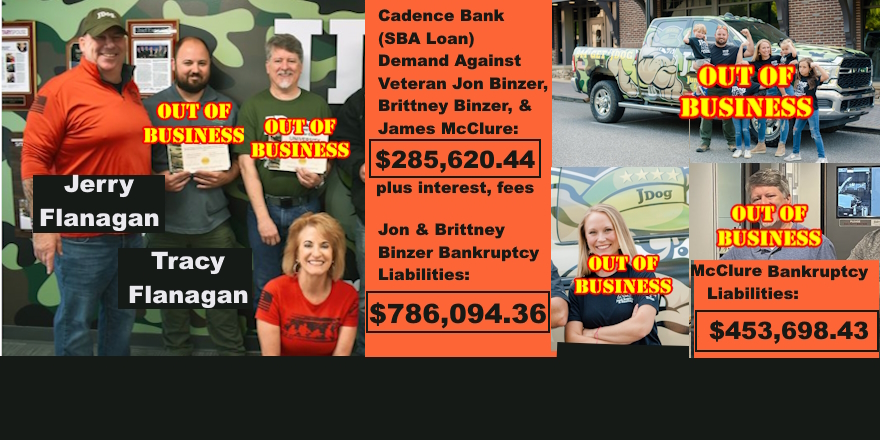

Marine Corps Veteran Jon Binzer lost $1.5M after investing in JDog Junk Removal and JDog Carpet Cleaning franchises. He and

Read More

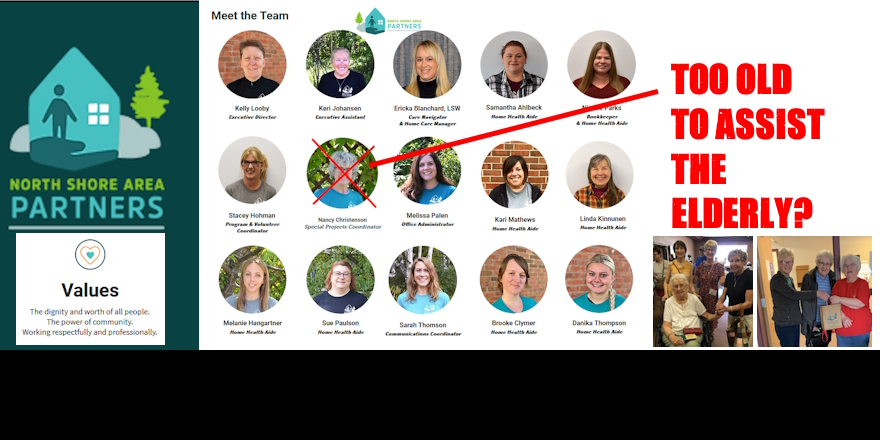

Minnesota Unkind: North Shore Area Partners & the Cruelty of Silent Age Discrimination by Sean Kelly Garrison Keillor helped establish

Read More

When serial entrepreneur and former franchisee Jim Lager decided to expand his successful hydraulic hose sales and repair into a

Read More

Many JDog franchise owners are relieved the Truth is coming out & Veterans are being warned. Others are angry that their

Read More

JDog Junk Removal & Hauling &JDog Carpet Cleaning & Floor Care franchisees claim to be dedicated to their fellow veterans,

Read MoreVeterans beware. You are the #1 prime target for scammers and exploiters. Fake News… Disinformation… Franchise scams… Lies… Ripoffs… Wolves

Read More

Sean Kelly, Franchise Truth founder & publisher of UnhappyFranchisee.Com, is reinventing the traditional folk music protest song to inform &

Read More